In 2025, more than 60% of pet parents said they would cut back on their own spending before touching their pet's care (MetLife / Talker Research). That single figure captures why pet health has become one of the most resilient growth markets in consumer, and why it is drawing brands, retailers, and investors all at once. Here is where the market is actually heading in 2026.

A large market that is still under-penetrated

The US pet wellness market now tops $5B (2025), roughly double many published figures that count only dog supplements and miss cat supplements, dental chews, and sprays and topicals (L.E.K. Consulting, NASC 2026). It has grown at a 14–15% CAGR since 2019, driven by real volume growth and premiumization rather than price inflation.

The striking part is how early it still is. Only about 20% of dogs and cats take a supplement consistently, well below human supplement use. Low penetration plus double-digit growth is exactly the combination that has investors moving in.

Spending that holds up in a downturn

Humanization is no longer a talking point; it is showing up in the wallet. 66% of pet parents splurge on high-quality food, 61% prioritize regular vet visits, and 37% expect to spend more on their pet in 2026 (MetLife / Talker Research). Average annual pet health spend reached $1,135 in 2025, up from $998 in 2024.

Demand also has a demographic tailwind. An estimated 35–40M pets adopted during the pandemic are now aging into their senior years, the period during which pet parents spend the most on health. Roughly two-thirds of pet parents say they will pay for life-extending products (Innova; NASC 2026).

Going to the shelf, before needing to go to the clinic

Where pet parents shop for health is shifting. Vet service prices are up 5.5% year over year (US BLS, April 2026), and clinic visits are declining as cost pressure pushes routine and preventive care off the exam table (GlobalPETS, June 2026).

The largest animal-health players are following pet parents to where they already shop. For functional ingredients, discovery and growth increasingly happen on the retail shelf, not in the clinic.

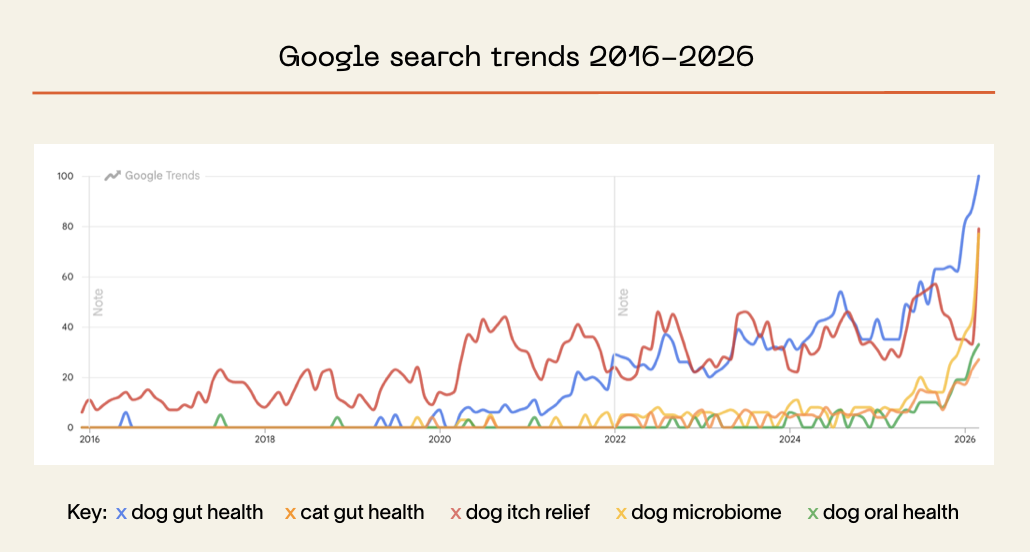

Pet parents are actively searching for answers

The demand is visible in real time. Over the past decade, US search interest in the exact need states functional ingredients address has climbed across the board, with sharp inflections over the past year (Google Trends, US, 2016–2026):

- Dog gut health search interest is up ~56% year over year, from virtually no search presence before 2020.

- Cat gut health searches grew ~165% year over year, from nearly zero in 2022.

- Dog microbiome is up ~270% (nearly 4x), from near zero as recently as 2024.

- Dog oral health is up ~210% (more than tripled) over the same window.

- Dog itch relief is the most established of the four and up ~30%, with a reliable spike every allergy season.

All five hit their highest recorded search interest in the most recent month. And these map directly to the largest need states in pet: digestive, skin and itching, and oral health. Functional nutrition has crossed from nice-to-have to essential, with 41% of pet parents now calling it essential (Innova 2025), and "clinically proven" ranking as the single most preferred claim in head-to-head testing (FoodScience, NASC 2026).

The cat opportunity is finally real

For years the category treated cats as secondary - the supplement category is still roughly 75% dog-oriented. That is ending. From 2019 to 2025, the kitten-to-puppy adoption ratio climbed from ~66% to ~99%, essentially one-to-one, as cat-owning households grew while dog-owning households declined (PetFoodIndustry, 2026). Over half of cat-owning households now include a cat over age 7, driving longevity demand.

And the demand is now showing up in search too: cat gut health search interest is up ~165% year over year, hitting its highest level on record last month (Google Trends, US, 2016–2026). The gap between where the pets are and where the products are is the clearest white space in pet health.

The bottom line

The macro picture is consistent across every one of these forces: a large, resilient, and under-penetrated market that is moving to the shelf, broadening to cats, and increasingly rewarding proof. The tailwinds are real. The differentiator is whether a product actually works.

That is where the market is separating. As pet parents grow more discerning and "clinically proven" becomes the claim they want most, the advantage goes to the brands whose ingredients can back the claims, with science and noticeable benefit delivery. Kingdom exists to put brands on the right side of that line. We create Superculture® ingredients: clinically validated postbiotics built for the exact need states this market is pulling toward, from gut and skin to oral health, in both dogs and cats.

Building for where pet health is heading? Get in touch with our team.